Best investment banks in Canada

The Royal Bank of Canada (NYSE: RY) is the largest Canadian bank by market capitalization, at ~$94 billion as listed on the NYSE. It were incorporated in 1869 as a regional bank, and has since grown to serve customers in Canada, the US, and 37 other countries. The bank's dividend streak is impressive, having paid steady or increasing dividends every year since 1943. It froze its dividend for 2 years through the financial crisis, and has increased it every year since 2010. RY's business segments are highlighted below:

The Royal Bank of Canada (NYSE: RY) is the largest Canadian bank by market capitalization, at ~$94 billion as listed on the NYSE. It were incorporated in 1869 as a regional bank, and has since grown to serve customers in Canada, the US, and 37 other countries. The bank's dividend streak is impressive, having paid steady or increasing dividends every year since 1943. It froze its dividend for 2 years through the financial crisis, and has increased it every year since 2010. RY's business segments are highlighted below:

Source: Investor Presentation

RY may be a global bank, but it still generates the lion's share (no pun intended) of its revenue at home in Canada. The bank is growing well in the US, including its recent acquisition of City National Bank, and it has an international segment comprising 17% of the business. RY carries a 10.3% Tier 1 Common Equity Capital Ratio, well above the 6% Basel III requirement, and in line with peers. This ratio is an important liquidity score that attempts to quantify a bank's ability to withstand stress. RY is well known for being a conservative and safe investment, primarily due to its performance through the Great Recession. Along with the other large Canadian banks, it was a relative safe harbor during a very rough time for financial stocks.

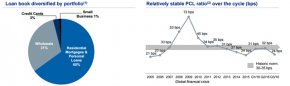

Loan Portfolio

Loan Portfolio

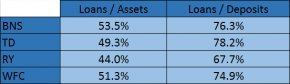

The table above shows the loans/assets and loans/deposits ratios of RY and its 2 largest Canadian competitors, The Bank of Nova Scotia (NYSE: BNS) and Toronto-Dominion Bank (NYSE: TD), as well as the Warren Buffett favorite Wells Fargo (NYSE: WFC). These ratios represent liquidity as well as the risk profile of a bank. Banks willing to hold more loans versus their total assets or deposits shows their tolerance for risk. These numbers can definitely be too high, but they can also be too low, showing a bank isn't driving the earnings growth it could. RY holds the lowest (most conservative) of both of these ratios by a sizable margin.

RY, like its competitor TD, carries a significant amount of loans in the real estate market. Home prices have been careening upwards in Canada (specifically in Toronto and Vancouver) to what are considered unsustainable levels. There is a widely held perception that this represents a bubble, and that any number of catalysts will cause the housing market to tank, causing distress for both these big mortgage banks. However, my take is that both of these banks are conservative, wide-moat businesses, and they will make it through a drop in their housing market just like they have made it through recessions and stock market crashes in the past.

However, my take is that both of these banks are conservative, wide-moat businesses, and they will make it through a drop in their housing market just like they have made it through recessions and stock market crashes in the past.

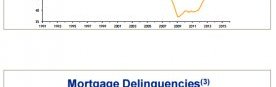

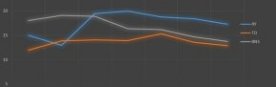

These graphs show the difference in the average Canadian homeowner versus an American one. The % of equity in their houses is much higher, and they have held a lower delinquency rate through the recent past. A lot of this has to do with more stringent regulations on mortgages in Canada. There are more requirements in regard to down payments, mortgage insurance and LTV (loan amount to house appraisal value). This makes a disaster less likely to occur, and RY is extremely conservative in nature.

Growth

RY's City National Bank acquisition closed late last year. This is expected to bolt-on and add to RY's footprint in America. It brings in over ~C2 billion in client-managed assets, swelling RY's wealth management and capital markets businesses. The company plans on leveraging CNB's positioning in the highest net worth locations in America to cross-sell RY products. This will give RY an additional growth opportunity in America, with access to a whole new client base. A bank this size has a huge amount of products to offer, and RY can use the customers it is gaining from CNB and future acquisitions to grow its revenues.

This will give RY an additional growth opportunity in America, with access to a whole new client base. A bank this size has a huge amount of products to offer, and RY can use the customers it is gaining from CNB and future acquisitions to grow its revenues.

Management has targeted a goal of 7%+ EPS growth over the next 5 years. Over the past 5 years, they have achieved a rate of ~12%. With the situation possibly brewing in Canada's housing market, it's possible that the company will achieve lower rates due to an increase in defaults going forward. However, 7% seems likely, and this would yield a total return of ~11%+ for investors.

Financials

RY carries the highest ROE by a substantial margin. The bank has targeted 18%+ going forward, and it has achieved that number in the past. One thing that should help it reach that goal is the buyback program I will detail later in the article. Significant increases in net income over the past several years have set RY apart from its main competitors in this regard.

Again, RY is the best of the 3 banks in ROA. This metric shows the ability of a bank to leverage its assets into earnings. This is another key profitability metric in RY's favor.

It has the worst net interest margin of the 3 banks. This metric is largely driven by interest rates. When interest rates do begin rising again - which they will at some point - banks will benefit, with their margins increasing.

RY has driven a good amount of FCF growth over the last several years. It is behind TD, which is an absolute FCF machine, but it's enough to service the ~C$7.4 billion in long-term debt the bank is currently carrying, and still increase its dividend. RY has targeted a 40-50% payout ratio, and it is currently at 46.40%. This means investors should expect the DGR to stabilize somewhere around the earnings growth rate going forward, which is expected to be ~7%+.